On mutually beneficial terms at time t1E a voluntary transaction is performed. Then the market sinks back into a dormant state until the next harvest and the next year's sale at time t2.

Let’s assume, for certainty, that the new season's crop has increased, so qS(t2)>qS(t1). In this case the seller obviously has to set the starting price lower right away, pS(t2) < pS(t1), while the buyer also takes the opportunity to lower the price and increase his amount of grain: pD(t2) < pD(t1) and qD(t2) > qD(t1). In this case it is natural to expect that the trajectories of the buyer and the seller will be slightly different, and the agreement between the buyer and the seller will be reached with different parameters than in the previous bidding round.

Conditionally, we will describe the situation in the market at each moment of time using a set of real market prices and quantities of real transactions that actually take place in the market. As can be seen from Fig. 1.3, in our model real transactions occur in the market only at such moments of time as t1E and t2E when the following market equilibrium conditions are true (points in Fig. 1.3)

1.6.3. CONCEPT OF SUPPLY AND DEMAND IN CLASSICS

In formulas (1.3)-(1.5) we used several new concepts and definitions that require some explanation. We will explain it in some detail, as it is important for understanding the subsequent presentation of the theory. First, the concept of S&D plays one of the central roles in modern economic theory. The same applies to probabilistic economic theory, which, as we said above, can to some extent be interpreted as a theory of supply and demand. Intuitively, on a qualitative descriptive level, all economists understand what this concept means. Difficulties and discrepancies appear only in practice when trying to give a mathematical interpretation of these concepts and to develop an adequate method for their calculation and measurement. For this purpose, various theories containing different mathematical models of S&D have been developed. These theories use various S&D functions to formally define and quantify S&D.

In this paper we will also repeatedly provide various mathematical representations of this concept within the framework of probabilistic economics, complementing each other. For example, in the framework of our two-agent classical economics (negotiation model) let’s represent the S&D functions as follows:

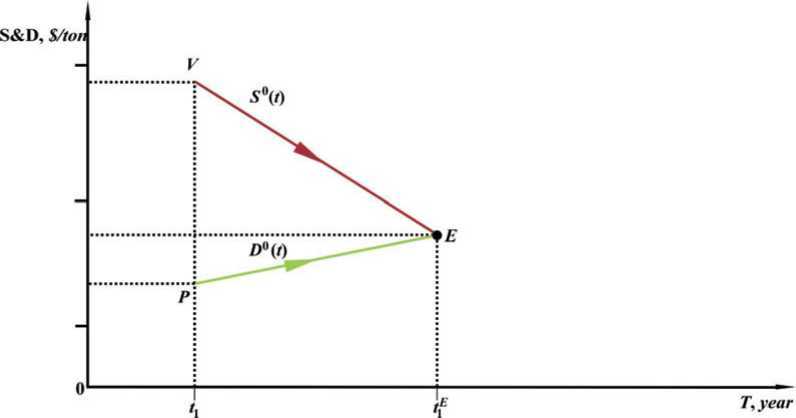

In equations (1.6) and (1.7), we have defined at each time t the total buyer demand function, D0(t) and the total seller supply function, S0(t), as the multiplication of price and quantity quotations. For brevity, we shall hereafter refer to them simply as supply and demand functions, i.e., we shall omit the word «total» unless this could lead to confusion. These functions can easily be depicted in the time and S&D coordinate system, namely: [T, S&D], as shown in Fig. 1.4, which shows a diagram of the complete S&D functions. As expected, the S&D functions also intersect at the equilibrium point E1. More strictly, the equilibrium point is exactly the point in the diagram where the price and quantity quotations of the buyer and seller are equal. The fact that the S&D functions are also equal at this point is a simple consequence of their definition and the equality of prices and quantities in this point.

The last remark concerns the formula for estimating the market trade volume (Trade Volume, hereafter TV) in the market TV (t1E) between a buyer and a seller at those moments in time when they come to a mutual understanding and conclude a transaction at an equilibrium point. Clearly, one can simply multiply the equilibrium values of price and quantity in this classical market model to obtain the trade turnover, or the total volume of all transactions, which follows from the above formula. The dimension of trade volume is the product of the dimensions of price and quantity; in our example, it is $. The same is true for the dimensions of the functions S&D, namely D0(t) и S0(t). Based on Fig. 1.4 we can conclude that it is at the equilibrium point that the trade volume reaches its maximum value. This result, which is self-evident and trivial in this case, is, in our opinion, rather general and principled: using it, we can deduce an assumption that markets tend to reach the equilibrium where maximum sales in monetary terms are achieved. It is possible to formulate this statement differently – in the form of the following hypothesis: markets strive for the maximum trading volume that is reached in equilibrium conditions, which agrees with the principle of trade volume maximization.

Fig. 1.4. Diagram of functions S&D, reflecting the dynamics of the classical two-agent market economy in the coordinate system [T, S & D] in the first time interval [t1,t1E].

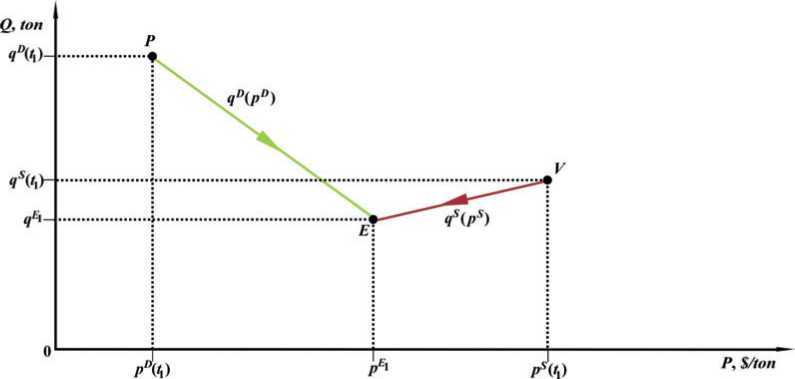

Further, similarly to classical mechanics, we can consider prices and quantities of market agents as trajectories of market agents in two-dimensional economic space using the coordinate system [P, Q] as shown in Fig. 1.5. Let us clarify that time t in this parametric representation of functions S&D is an implicit parameter. Generally, this parametric representation gives nothing new compared to Figs. 1.3 and 1.4. Nevertheless, there is one interesting nuance here – the similarity of this diagram with the traditional picture in the neoclassical S&D model, namely the Marshall cross. We will touch on this issue a little later, but for now let's look at some of the features in Fig. 1.5. First, as the arrows show, the buyer and the seller move toward each other in terms of price: the seller lowers it, and the buyer, on the contrary, raises it. Thus the figure reflects normal market negotiation processes. Second, usually during negotiations, quantity quotations are reduced by both agents, i.e. both the buyer and the seller.

Fig. 1.5. Dynamics of the classical two-agent market economy in the two-dimensional economic space of price-quantity in the first time interval [t1,t1E].

Clearly, all agents want to buy or sell less goods at a compromise market price than at the desired prices they stated at the beginning of the trade. These factors together determine that the slope of the demand curve qD(pD) is negative and the slope of the supply curve qS(pS) is positive, just as the S&D functions in the neoclassical model «should» be. But this visual similarity is incomplete, because the economic meaning of these pictures in the two theories differs significantly: in the classical model it is a description of the actual process of negotiations in order to reach a deal, and in the neoclassical model it is a description of strategies of behavior of agents in the market in terms of neoclassical supply and demand curves, qD(pD) and qS(pS). We emphasize that while in neoclassics these curves, by definition, represent as it were the actual functions of supply and demand, in classics these curves are simply a graphical representation of the price and quantitative time trajectories in the form of one trajectory in the course of trading. Thus, the classic economic theory does not assume the existence of any definite dependence of the agents’ quantitative quotations on price quotations, i.e. the existence of any definite functions qD(pD) and qS(pS).